Missouri Homeowners Insurance Quotes

Everything You Need to Know About Home Insurance in Missouri

Missouri presents a wide mix of living environments, from energetic urban centers and historic riverfront districts to expansive farmland and wooded lake communities that appeal to homeowners seeking both accessibility and space. Cities such as St. Louis and Kansas City feature dense neighborhoods with older masonry construction, while suburban corridors and rural counties often include newer single-family homes, manufactured housing, and multi-acre properties. This architectural and geographic diversity means homeowners insurance needs rarely look the same from one ZIP code to the next, as construction materials, square footage, and proximity to emergency services can all influence policy structure and pricing.

The state also encounters a broad range of seasonal weather conditions that shape insurance planning. Spring tornado systems, intense summer thunderstorms, winter ice accumulation, and periodic flooding along rivers and low-lying terrain can all affect rebuilding expenses and deductible requirements. Even homes outside major flood zones may review drainage or water-backup coverage due to localized rainfall patterns. Because material costs, labor rates, and weather frequency continue to evolve, maintaining adequate home insurance coverage in Missouri is an important part of long-term financial protection.

How Much Does Homeowners Insurance Cost in Missouri?

The average cost of homeowners insurance policies in the state is approximately $2,850 per year, or about $238 per month, for a home insured with $300,000 in dwelling coverage. This figure is higher than the national average, largely due to the state’s exposure to severe thunderstorms, hail, and tornado activity that can lead to costly roof and structural claims. Construction material pricing and labor shortages in certain regions have also contributed to gradual premium increases over recent years.

Insurance pricing is not uniform across the state, and ZIP code plays a significant role in determining final costs. Urban properties, older homes, and residences near flood-prone waterways may experience different underwriting guidelines than newer suburban developments.

How to Find Home Insurance in Missouri

Finding the right home insurance policy often begins with evaluating how regional weather exposure and rebuilding costs influence carrier availability. Homes in tornado-active counties or flood-adjacent zones may require additional endorsements or separate policies, while inland suburban neighborhoods often have broader insurer participation. Reviewing multiple insurance quotes side-by-side helps homeowners compare deductible structures, dwelling limits, and optional protections in a single view rather than navigating separate applications.

Risk-reduction improvements can also influence long-term eligibility and pricing. Upgraded roofing materials, reinforced garage doors, modernized electrical systems, and improved drainage around foundations may support more favorable underwriting outcomes. Independent agencies such as InsureOne streamline the search process by presenting policy options from several insurers simultaneously, allowing residents to focus on coverage alignment rather than brand limitations.

How Do Home Insurance Deductibles Affect Rates in Missouri?

Deductibles are the amount a homeowner agrees to contribute toward a covered repair before insurance coverage begins, and they have a direct influence on premium amounts. Selecting a higher deductible typically lowers yearly policy costs because the homeowner assumes more financial responsibility upfront, while choosing a lower deductible usually increases monthly premiums but reduces immediate out-of-pocket expenses when a claim is filed.

For example, if a homeowner selects a $2,500 deductible and incurs $10,000 in wind damage, the insurer would typically cover $7,500 once the deductible is met, subject to policy limits. In storm-active regions, some carriers may apply separate wind or hail deductibles based on geographic exposure, which can differ from the standard deductible listed on the declarations page.

Compare Home Insurance Rates by Coverage Levels in Missouri

Dwelling coverage is based on projected rebuilding expenses rather than real-estate market value, and premiums generally increase as coverage limits rise. Homes with older construction, custom features, or multi-unit layouts may require higher restoration budgets, which can influence insurance pricing. The table below reflects statewide averages rather than exact neighborhood-level quotes. Reviewing a range of Missouri home insurance quotes helps clarify how pricing may vary by property details.

| Dwelling Coverage | Average Annual Insurance Cost |

|---|---|

| $100,000 | $1,020 |

| $200,000 | $1,690 |

| $300,000 | $2,850 |

| $400,000 | $3,620 |

| $500,000 | $4,410 |

Is Home Insurance Tax Deductible in Missouri?

For most primary residences, home insurance premiums are not tax deductible because they are considered personal living expenses under federal tax guidelines. There are, however, limited scenarios where portions of insurance costs or related losses may qualify depending on how the property is used and how the loss occurred. Because eligibility depends on individual filing status and documentation, professional tax guidance is strongly recommended before applying deductions.

Situations where partial deductions may apply include:

- A designated home office used exclusively for business purposes

- Rental income generated from a portion of the property

- Federally declared disaster losses that were not fully reimbursed by insurance

- Certain casualty-loss claims tied to qualifying natural events

Tax laws change periodically, and qualification thresholds can shift from year to year, which is why homeowners should verify current requirements before making assumptions about deductibility.

Does Missouri Have the 80% Homeowners Insurance Rule?

Most insurance carriers apply the 80% rule when evaluating claim reimbursements for Missouri homeowners insurance policies. This guideline means the dwelling coverage limit should equal at least 80% of the estimated replacement cost of the home to receive full payment for covered structural losses.

For instance, if rebuilding a property is estimated at $400,000, maintaining at least $320,000 in dwelling coverage helps prevent partial reimbursement penalties. Replacement costs can fluctuate due to material pricing, labor demand, and renovations, which makes periodic coverage reviews important. Homeowners who reassess limits annually are more likely to maintain alignment with current rebuilding expenses.

Bundling Home and Auto Insurance in Missouri

Many residents choose to bundle home insurance in Missouri with auto coverage to simplify policy management and potentially reduce overall insurance expenses. Multi-policy discounts often align billing cycles, centralize claims handling, and help maintain consistent liability limits across policies so coverage gaps are less likely to occur. In addition to potential savings, bundling can make renewals and documentation easier to track because homeowners are working with a single insurer instead of multiple companies. Some carriers also offer loyalty incentives or enhanced deductible options for customers who maintain several active policies.

Bundling opportunities may extend beyond home and auto to include motorcycles, recreational vehicles, boats, or personal umbrella policies depending on insurer offerings and eligibility guidelines. Homeowners with multiple insured assets frequently find that consolidating coverage provides clearer visibility into total insurance costs over time. With InsureOne, Missouri property owners can compare bundled home insurance quotes side-by-side to identify policies that deliver meaningful value without sacrificing dependable coverage.

What Factors Do Insurers Consider in Missouri?

Insurance carriers evaluate a combination of structural details, geographic exposure, and rebuilding costs when determining homeowners insurance rates. Core considerations include the home’s location, construction materials, age of the property, roof condition, and proximity to fire hydrants or fire stations because these elements influence emergency response time and potential repair expenses. Credit history and prior claims activity are also commonly reviewed, as they help insurers estimate future risk and underwriting eligibility. Replacement-cost calculations based on local labor rates and material pricing further shape final premium amounts.

Beyond these standard factors, Missouri-specific risks also influence pricing decisions. Properties located in central and western portions of the state may be evaluated for tornado corridor exposure, while homes near rivers or low-lying landforms can fall into higher flood-risk categories. Seasonal hailstorms, strong thunderstorms, and winter ice accumulation may affect deductible structures and roof-related underwriting guidelines. Portions of southeastern Missouri are also assessed for occasional seismic exposure, and local building code requirements or updated construction standards can increase reconstruction expenses following a covered loss.

What Weather Affects Home Insurance Costs in Missouri?

Missouri’s geographic position exposes homeowners to several weather patterns that can influence insurance pricing and deductible structures.

- Tornadoes and Severe Thunderstorms: Spring and early summer storms frequently bring high winds and hail capable of causing roof and siding damage.

- Flooding: River systems and heavy rainfall can create localized flood risks, which typically require separate flood insurance coverage.

- Winter Ice and Snow: Freezing temperatures may contribute to burst pipes, ice dams, and structural strain on roofing systems.

- Occasional Seismic Activity: Portions of southeastern Missouri sit near the New Madrid Seismic Zone, prompting some homeowners to evaluate optional earthquake endorsements.

Understanding these regional influences helps residents determine whether additional protections or policy endorsements are appropriate for their property type and location.

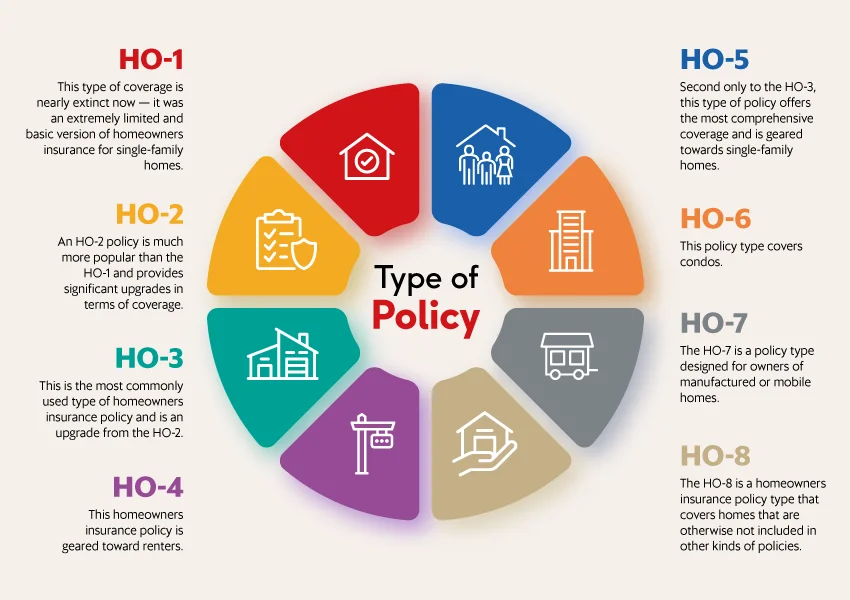

What Are the Different Types of Home Insurance?

Home insurance policies are organized through standardized HO forms that correspond to ownership structure and property type rather than architectural style alone. The HO-3 policy is the most commonly selected option for single-family homes because it provides broad dwelling protection alongside defined personal property coverage. Homeowners seeking expanded personal belongings protection may consider HO-5 coverage, while condominium owners typically rely on HO-6, renters use HO-4, and manufactured homes often require HO-7 policies due to construction differences.

Local homeowners frequently evaluate endorsements such as water-backup coverage, ordinance or law protection for code upgrades, and extended replacement cost options. Reviewing both policy form and endorsements ensures alignment with regional weather exposure and structural characteristics rather than relying on a one-size-fits-all approach.

What Is the Most Common Homeowners Insurance in Missouri?

The HO-3 homeowners policy remains the most widely used form of homeowners insurance residents select because it balances structural protection with personal property coverage and liability safeguards. While HO-3 policies work for most detached houses, coverage needs can vary based on property age, materials, and geographic exposure. Homes in tornado-active regions may review wind deductibles, while river-adjacent properties often evaluate flood endorsements or separate flood policies. Understanding regional risks allows homeowners to adjust coverage limits and optional protections more precisely.

Get the Best Homeowners Insurance in Missouri Today

Securing home insurance in Missouri often centers on evaluating structural coverage, environmental exposure, and financial planning goals. InsureOne consolidates options from various insurance providers into one organized view to support data-driven decisions.

Get started with a quick online quote, speak with a licensed insurance professional by phone at 800-836-2240, or visit a local office for personalized assistance. With access to several carriers and customizable coverage structures, InsureOne helps Missouri residents secure protection that aligns with both property value and regional risk conditions.

FAQs

How Much Is Homeowners Insurance in Missouri?

Homeowners insurance rates in Missouri often trend above the national average, largely influenced by storm frequency and rising construction costs. Pricing can differ widely by ZIP code, roof age, and property condition rather than following a single statewide figure. Homes near rivers or dense urban centers may see different premium structures than suburban or rural residences.

Is Home Insurance Required in Missouri?

While the state does not obligate every property owner to purchase insurance, most banks require it as part of a mortgage agreement. Home insurance in Missouri still plays an important role for owners without loans by helping cover rebuilding costs, legal liabilities, and short-term housing needs after a loss. Unexpected weather events or accidents can generate significant expenses. Coverage acts as a practical layer of financial protection, not just a formal requirement.

What Weather Risks Affect Home Insurance in Missouri?

Insurance pricing is heavily influenced by tornado activity, hailstorms, heavy rainfall, and winter freezing conditions. Certain counties may also review seismic exposure due to proximity to regional fault zones. Flood damage is not included in standard homeowners policies and usually requires a separate flood insurance plan. These factors collectively shape deductible structures and overall homeowners insurance premiums.

What Factors Influence Home Insurance Rates in Missouri?

Insurance carriers evaluate construction materials, roof age, property location, and estimated rebuilding costs when determining pricing. Claims history and proximity to fire services can also influence eligibility and premium calculations. Homes with upgraded roofing or modern electrical systems may qualify for more favorable underwriting outcomes.