Michigan Homeowners Insurance Quotes

Everything You Need to Know About Home Insurance in Michigan

Homeownership in Michigan often comes with a unique mix of waterfront living, historic neighborhoods, and suburban expansion that shapes how insurance coverage is selected. Many residents own properties near inland lakes or along the Great Lakes shoreline, while others live in older industrial-era homes or newly built communities outside major cities. These differences in architecture, age, and location can influence rebuilding costs, maintenance needs, and policy requirements. Detached garages, basements, and seasonal cottages are also common features that affect coverage limits and endorsements.

Climate conditions further distinguish homeowners insurance in Michigan from other regions. Extended winters bring heavy snow accumulation, freezing temperatures, and the potential for ice dams, while warmer months may introduce windstorms, hail, and localized flooding near rivers or shorelines. Because geographic exposure shifts throughout Michigan, checking quotes from different insurers supports coverage decisions that account for both property design and location-specific risks.

How Much Does Homeowners Insurance Cost in Michigan?

The average cost of home insurance in Michigan is approximately $1,580 per year, or about $132 per month for $300,000 in dwelling coverage. While premiums remain close to national averages, several market trends have contributed to gradual increases, including higher construction material pricing, skilled labor shortages, and greater demand for repairs following winter storms.

Pricing also varies by ZIP code due to regional rebuilding expenses and differences in snowfall intensity or lake-effect weather patterns. Evaluating multiple home insurance Michigan quotes provides clearer insight into location-specific costs and available discounts.

Does Michigan Have the 80% Homeowners Insurance Rule?

Most insurers in Michigan apply the 80% homeowners insurance rule when calculating reimbursement after a covered loss. This guideline generally requires policyholders to insure their dwelling for at least 80% of its estimated replacement cost to qualify for full claim payment. Replacement cost reflects the expense of reconstructing the home using comparable materials rather than its market resale value.

Falling below this level can result in partial payouts even when damage is not total, which is why periodic coverage reviews are important after renovations or material price increases.

How to Find Home Insurance in Michigan

Securing property insurance in Michigan is typically straightforward for newer homes in lower-risk areas, but older structures or lake-adjacent properties may require additional comparison. Working with an agency that can compare home insurance quotes in Michigan often increases both pricing transparency and carrier availability.

Homeowners who encounter underwriting restrictions may also explore the Michigan FAIR Plan, which serves as a safety-net coverage option for qualifying properties. Reviewing policies from multiple insurers ensures broader visibility into deductible structures, endorsements, and rebuilding cost calculations.

Risk-reduction improvements can also influence eligibility and long-term premiums. Common upgrades include improving attic insulation to reduce ice dam risk, installing sump pumps in basements, updating roofing materials, and reinforcing drainage systems around foundations. These preventative measures not only support more favorable underwriting outcomes but can also minimize the likelihood of future claims.

How Do Home Insurance Deductibles Affect Rates in Michigan?

Deductibles represent the portion of repair costs a homeowner agrees to pay before insurance coverage applies after an approved claim. Choosing a higher deductible typically lowers annual premiums because the homeowner assumes more financial responsibility, while lower deductibles increase monthly expenses but reduce immediate out-of-pocket costs when damage occurs.

Some home insurance Michigan policies may include separate wind or hail deductibles depending on regional storm exposure, insurer guidelines, and the age or condition of the roof. These deductible structures can vary by ZIP code and carrier, which is why reviewing policy details carefully is important.

Determining the right deductible often involves evaluating both financial preparedness and long-term premium savings. Homeowners may consider emergency savings, the likelihood of filing smaller claims, and the overall value of the property when making this decision. Selecting a deductible that is too low can raise yearly costs, while one that is too high may create financial strain during unexpected repairs.

Compare Home Insurance Rates by Coverage Levels in Michigan

Dwelling coverage reflects the estimated cost to rebuild the home rather than its market value, and premiums increase as coverage limits rise. Michigan properties with basements, detached structures, or proximity to water may experience higher pricing due to restoration complexity. The table below illustrates general statewide averages rather than exact ZIP-code quotes.

| Dwelling Coverage | Average Annual Insurance Cost |

|---|---|

| $150,000 | $840 |

| $250,000 | $1,190 |

| $300,000 | $1,580 |

| $400,000 | $1,960 |

| $500,000 | $2,420 |

Our average auto policy costs are based on a male driver, aged 30, with a clean driving record. Liability insurance coverage is the state‑required minimum. Full coverage is based on a 100K/300K/100K policy. Your costs will depend on your individual circumstances.

Is Home Insurance Tax Deductible in Michigan?

Homeowners insurance is generally not tax deductible for primary residences because it is classified as a personal living expense rather than a business cost. However, certain exceptions may apply depending on how the property is used and how income is reported. For example, if a portion of the home is used exclusively and regularly as a dedicated home office, a percentage of related housing expenses — including insurance — may qualify under federal tax rules. Similarly, properties that generate rental income or are partially leased to tenants may treat insurance premiums differently for tax purposes.

In limited situations, unreimbursed casualty losses resulting from federally declared disasters may also be eligible for deductions, although strict documentation and eligibility requirements typically apply. Tax regulations can change from year to year and often depend on filing status, income thresholds, and the classification of the property. Because these guidelines are complex and highly individualized, Michigan homeowners are generally encouraged to consult a licensed tax advisor or accountant before making deduction decisions related to homeowners insurance.

Bundling Home and Auto Insurance in Michigan

Many property owners choose to bundle home and auto policies to simplify billing and potentially reduce overall insurance expenses. Multi-policy discounts can align renewal dates, centralize claims management, and help maintain consistent liability limits. Multi-policy discounts occasionally extend beyond home and auto to umbrella or recreational vehicle insurance. InsureOne enables side-by-side bundle reviews so protection levels and financial value can be assessed together.

What Factors Do Insurers Consider in Michigan?

When determining home insurance rates in Michigan, insurers review both structural and environmental variables that influence claim likelihood and repair costs. Property characteristics and regional exposure play a central role in underwriting decisions, which is why pricing may differ even between nearby neighborhoods.

Key considerations include:

- Roof age and construction materials

- Presence of basements or detached structures

- ZIP-code claim frequency and local weather exposure

- Estimated rebuilding cost based on labor and materials

- Credit-based insurance score where permitted

- Safety features such as alarms or water shut-off devices

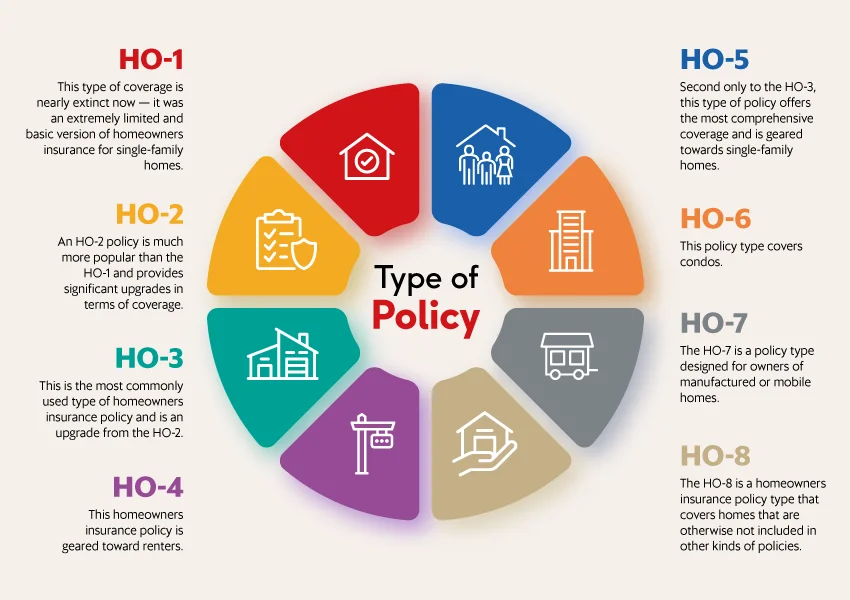

What Are the Different Types of Home Insurance?

Home insurance policies are categorized using standardized HO forms designed for various ownership and property types. The HO-3 policy remains the most common choice for single-family homes because it provides broad structural coverage alongside defined personal property protection. Homeowners seeking expanded protection may consider an HO-5 policy, while condominium owners typically use HO-6, renters rely on HO-4, and older or historically significant properties may require HO-8 valuation methods.

Many residents choose to customize their base insurance with endorsements designed for regional concerns. Water-backup options, code-upgrade coverage, and extended replacement protections are common choices, particularly for houses with lower levels or aging infrastructure. Looking at both the main policy and available add-ons makes it easier to match coverage to the home and local weather patterns.

What Is the Most Common Homeowners Insurance in Michigan?

Many Michigan homeowners select an HO-3 policy since it provides a strong mix of protection and affordability. Still, coverage needs differ depending on whether the property sits near water, in a city neighborhood, or in a snow-heavy region. Urban households often consider sump-pump or water-backup options, while rural and lakefront homes may focus more on outbuilding protection.

What Weather Affects Home Insurance Costs in Michigan?

Seasonal weather patterns significantly influence insurance pricing throughout Michigan. Heavy winter snowfall can place stress on roofs and increase the likelihood of ice dam formation, while spring storms may introduce wind and hail damage. Summer thunderstorms and localized flooding near rivers or lakes also contribute to claim frequency in certain regions. Evaluating these seasonal risks helps homeowners determine whether endorsements or separate flood coverage are appropriate.

What Does Homeowners Insurance Cover in Michigan?

Standard homeowners insurance policies in Michigan provide layered protection that extends beyond the building itself. Coverage typically applies to structural damage from covered perils as well as personal belongings and financial liability related to on-property incidents. Policy limits and deductibles influence reimbursement levels, making periodic reviews important as rebuilding costs change. Flood damage remains excluded and requires a separate flood insurance policy.

Most policies commonly include:

- Dwelling coverage for the home’s structure and attached systems

- Personal property coverage for interior belongings

- Liability protection for certain injury or property damage claims

- Additional living expenses (ALE) during covered repairs

- Other structures coverage for detached garages or sheds

Get the Best Homeowners Insurance in Michigan Today

Shopping for Michigan homeowners insurance is about more than price — it’s also about coverage strength and planning ahead. InsureOne helps by gathering multiple carrier options in one place, making side-by-side comparisons easier and faster.

Homeowners can begin with a quick online quote, visit a nearby office for in-person assistance, or call 800-836-2240 to speak with a licensed insurance professional. With InsureOne, Michigan residents gain access to informed guidance and coverage solutions designed to reflect the state’s diverse property styles and climate conditions.

FAQs

How much is homeowners insurance in Michigan?

The average cost of homeowners insurance in Michigan is about $1,580 per year, although pricing varies by ZIP code, home age, and rebuilding expenses. Waterfront properties or homes with older roofing materials may experience higher premiums. Seasonal weather exposure also influences annual rates.

Is homeowners insurance required in Michigan?

Michigan law does not mandate homeowners insurance for owner-occupied properties. However, mortgage lenders typically require a policy to protect their financial interest in the home. Even without a loan, many homeowners carry insurance because repair or rebuilding expenses after storms or fires can be substantial. Carrying homeowners insurance in Michigan provides protection for rebuilding costs and third-party liability claims.

What weather risks affect Michigan home insurance rates?

Insurance premiums in the state are influenced by heavy winter snowfall, freezing temperatures, and spring or summer thunderstorms. Ice dams, roof stress, and hail damage are common seasonal concerns. Flooding near lakes or rivers requires separate coverage because it is not included in standard policies. Insurers assess these risks carefully when determining home insurance rates in Michigan.

What factors influence the cost of homeowners insurance in Michigan?

Insurers evaluate location, home age, building materials, and estimated replacement cost when calculating premiums. Additional factors include roof condition, deductible selection, prior claims history, and local building codes. Environmental exposure such as lake-effect snow or flood zones may also influence pricing.