Maryland Homeowners Insurance Quotes

Everything You Need to Know About Home Insurance in Maryland

Maryland offers an uncommon blend of environments in a relatively compact space — waterfront communities along the Chesapeake Bay, historic city neighborhoods, growing suburban corridors near Washington, D.C., and quieter mountain regions to the west. Because housing styles and rebuilding costs shift so dramatically from county to county, homeowners insurance in Maryland is rarely uniform. A brick rowhome in Baltimore, a coastal cottage near Annapolis, and a newer townhouse outside Silver Spring each carry different structural considerations and risk profiles. Understanding how these property differences influence coverage is an important first step.

Seasonal weather patterns also play a role in insurance planning. Summer thunderstorms, winter ice accumulation, and localized flooding near rivers or low-lying areas can affect maintenance costs and long-term premiums. Rather than relying on generalized estimates, many residents review multiple Maryland homeowners insurance quotes to see how location, dwelling size, and deductible selections shape policy pricing. Comparing options allows homeowners to build coverage that reflects both the structure of the property and the environment surrounding it.

How Much Does Homeowners Insurance Cost in Maryland?

The average cost of home insurance in the state is approximately $1,780 per year for a policy with $300,000 in dwelling coverage, which is close to the national average but can vary by region. Coastal and densely populated counties may experience slightly higher premiums due to rebuilding demand and weather exposure, while inland areas sometimes see more moderate pricing. Dwelling coverage is calculated using the projected cost to reconstruct the home rather than its resale value, which is why two houses with similar market prices may carry different insurance costs.

Premiums also reflect factors such as roof condition, construction materials, prior claims history, and proximity to emergency services. Because these elements differ from one ZIP code to another, reviewing several homeowners insurance quotes often provides a clearer picture of personalized pricing than statewide averages alone.

How to Find Home Insurance in Maryland

Finding the right home insurance in Maryland often begins with understanding how location and property characteristics influence availability and pricing. Homes near the Chesapeake Bay, riverfront communities, or densely populated suburbs may encounter different underwriting guidelines than inland or rural properties.

Comparing insurance quotes from multiple carriers helps identify coverage limits, deductibles, and endorsements that align with both structural value and regional weather exposure. Because rebuilding costs and insurer participation can shift over time, reviewing options annually can prevent gaps in protection.

Residents may also benefit from evaluating risk-reduction measures such as updated roofing materials, modern electrical systems, or improved drainage around foundations. These improvements can influence eligibility and long-term premiums, particularly for older homes or multi-unit dwellings. Independent agencies like InsureOne simplify the process by presenting several policy options side-by-side rather than limiting homeowners to a single carrier. This approach supports informed decisions based on coverage structure, not just price.

How Do Home Insurance Deductibles Affect Rates in Maryland?

A deductible represents the portion of a covered loss a homeowner agrees to pay before insurance coverage applies, and it has a direct impact on annual premiums. Higher deductibles typically reduce monthly or yearly costs because the policyholder assumes more financial responsibility, while lower deductibles increase premiums but decrease out-of-pocket expenses after a claim. For example, choosing a $2,500 deductible instead of a $1,000 deductible may noticeably lower premium costs, but it also means paying more upfront if repairs are needed.

In certain coastal or storm-exposed areas, insurers may apply separate wind or percentage-based deductibles depending on risk guidelines. Evaluating deductible options side-by-side through multiple quotes allows residents to balance affordability with financial preparedness.

Compare Home Insurance Rates by Coverage Levels in Maryland

Dwelling coverage is based on estimated rebuilding costs rather than market value, and insurance premiums generally increase as coverage limits rise. Homes with specialized materials, historic elements, or multi-unit layouts may require higher restoration budgets. The table below reflects broad statewide averages rather than precise ZIP-code pricing, which is why individualized quotes remain important.

| Dwelling Coverage | Average Annual Insurance Cost |

|---|---|

| $100,000 | $840 |

| $200,000 | $1,240 |

| $300,000 | $1,780 |

| $400,000 | $2,320 |

| $500,000 | $2,910 |

Is Home Insurance Tax Deductible in Maryland?

For most primary residences, homeowners insurance is not tax deductible because it is considered a personal living expense. Exceptions may apply if a portion of the home is used exclusively for business purposes or if the property generates rental income. In limited circumstances, unreimbursed losses from federally declared disasters may qualify under current tax guidelines. Because eligibility varies based on filing status and property use, consulting a qualified tax professional is recommended.

Does Maryland Have the 80% Homeowners Insurance Rule?

Many insurance carriers apply what is commonly referred to as the 80% rule, an industry standard rather than a state mandate. This guideline means a homeowner should carry dwelling coverage equal to at least 80% of the home’s estimated replacement cost to receive full reimbursement after a covered loss. If coverage falls below that threshold, claim payments may be reduced even for partial damage.

Rebuilding expenses can shift due to renovation projects, material price changes, or labor demand, so reviewing dwelling limits periodically is important. Comparing home insurance quotes in Maryland helps ensure coverage remains aligned with current construction costs rather than outdated estimates.

Bundling Home and Auto Insurance in Maryland

Many residents bundle home and auto insurance to simplify policy management and potentially lower overall insurance expenses. Multi-policy discounts can align billing cycles, centralize claims administration, and maintain consistent liability limits across coverage lines. Bundling opportunities may also extend to umbrella policies, recreational vehicles, or watercraft depending on carrier offerings.

Rather than focusing solely on discounts, residents often evaluate how bundled coverage affects long-term protection and policy organization. Reviewing bundled Maryland homeowners insurance quotes side-by-side allows residents to weigh both cost efficiency and coverage structure.

What Factors Do Insurers Consider in Maryland?

Insurance pricing in the region reflects both structural and environmental variables that influence claim likelihood and repair costs. Because coastal and inland regions present different exposure profiles, pricing may vary even between nearby communities.

Key considerations include:

- Proximity to coastline, rivers, or flood zones

- Roof age and exterior materials

- ZIP-code claim frequency and storm exposure

- Estimated rebuilding cost based on labor and materials

- Credit-based insurance score where permitted

- Presence of safety features such as alarms or water shut-off systems

What Weather Affects Home Insurance Costs in Maryland?

Weather exposure varies across the state and plays a measurable role in premium calculations. Coastal counties evaluate wind and tidal flooding risks, while inland regions may focus more on thunderstorms, hail, and winter ice accumulation. Snow load, frozen pipes, and tree-related damage are common winter considerations, particularly for older properties with aging infrastructure. Heavy rainfall near rivers or bays can also increase the need for separate flood coverage, which is not included in standard homeowners policies.

Understanding how these seasonal influences intersect with property location helps property owners determine whether endorsements or higher dwelling limits are appropriate for their coverage strategy.

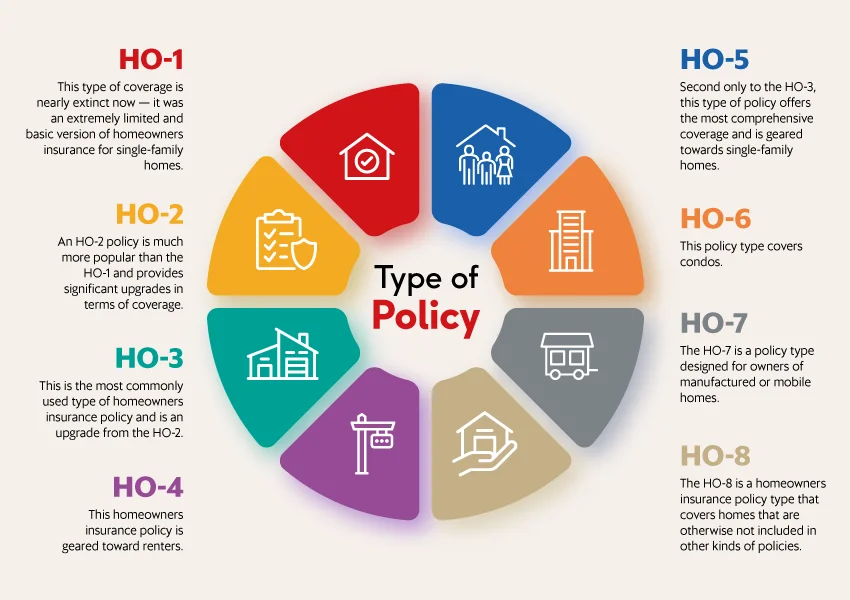

What Are the Different Types of Home Insurance?

Home insurance policies are organized through standardized forms that correspond to ownership structure and property type. The HO-3 policy remains the most widely used option for single-family homes because it offers broad structural protection along with defined personal property coverage. Homeowners seeking expanded personal property protection may consider an HO-5 policy, while condominium owners typically rely on HO-6 coverage, renters use HO-4, and manufactured homes often require HO-7 policies.

Policy selection is frequently influenced by building age, renovation history, and proximity to water or dense urban areas. Evaluating both base policy form and optional endorsements ensures alignment with property characteristics rather than relying on a generic template.

What Is the Most Common Homeowners Insurance in Maryland?

The HO-3 policy is the most common homeowners insurance format because it balances structural protection with practical personal property coverage. It insures the dwelling against a wide range of risks while providing named-peril coverage for belongings, liability protection, and additional living expenses after covered losses. While HO-3 suits many detached homes, properties with historic features or uncommon materials sometimes evaluate modified or extended replacement options to reflect restoration needs.

Coverage selection often depends on property design and neighborhood density rather than state-wide norms, which is why reviewing multiple quotes remains a common step in the decision-making process.

Get the Best Homeowners Insurance in Maryland Today

Securing homeowners insurance in Maryland is less about finding a single price and more about building coverage that reflects how and where you live. InsureOne reviews multiple carriers, organizes options clearly, and helps residents move from comparison to confidence without unnecessary complexity. Whether starting with a quick online quote, by calling 800-836-2240, or visiting a nearby office, homeowners gain access to flexible policy structures and knowledgeable guidance tailored to their property profile.

With organized comparisons and multiple insurer options, Maryland residents can focus less on navigating insurance logistics and more on maintaining the long-term protection of their homes.

FAQs

How Much Is Homeowners Insurance in Maryland?

The average cost of homeowners insurance in Maryland typically falls slightly below the national average, but actual pricing depends heavily on ZIP code, home age, and rebuilding costs. Waterfront properties or homes in flood-prone areas may experience higher premiums due to increased exposure. Inland suburban communities often see more moderate pricing structures. Comparing multiple insurance quotes remains the most accurate way to estimate personalized rates.

Is Home Insurance Required in Maryland?

Maryland law does not mandate homeowners insurance for all property owners, but most mortgage lenders require active coverage as a loan condition. Even without a mortgage, maintaining home insurance protection helps safeguard against structural damage, liability claims, and temporary living expenses after a loss. Severe weather, fire incidents, and water damage can result in significant repair costs. Insurance acts as a financial safety layer rather than a legal obligation.

What Weather Risks Affect Home Insurance in Maryland?

Insurance pricing in the state is influenced by a blend of coastal and inland weather patterns rather than a single dominant threat. Heavy rain, localized flooding, winter snow accumulation, and seasonal thunderstorms are frequent underwriting considerations. Coastal communities may also review wind exposure and storm surge risk when evaluating coverage options. These variables can impact deductibles, endorsements, and overall homeowners insurance premiums.

Insurance pricing in the state is influenced by a blend of coastal and inland weather patterns rather than a single dominant threat. Heavy rain, localized flooding, winter snow accumulation, and seasonal thunderstorms are frequent underwriting considerations. Coastal communities may also review wind exposure and storm surge risk when evaluating coverage options. These variables can impact deductibles, endorsements, and overall homeowners insurance premiums.

Insurance carriers assess multiple elements when calculating policy holder pricing, including construction materials, roof age, and proximity to fire services. Location plays a central role, especially for homes near waterways or in dense metropolitan corridors. Claims history and rebuilding cost estimates further shape premium calculations.