Massachusetts Homeowners Insurance Quotes

Everything You Need to Know About Home Insurance in Massachusetts

Massachusetts homeowners often balance dense urban living with coastal exposure and historic architecture rather than wide suburban sprawl. A brownstone in Boston, a Cape-style home on the South Shore, and a colonial property in Worcester can all carry different rebuilding requirements even within the same county. Many houses include older masonry, finished attics, or multi-family layouts that influence replacement cost calculations and endorsement needs. Because the state contains both shoreline communities and inland towns with aging housing stock, homeowners insurance in Massachusetts is frequently shaped by property age and construction style as much as location.

Seasonal weather and coastal influence add another dimension to insurance planning. Nor’easters, winter ice accumulation, and occasional tropical storm remnants can affect roofing systems, basements, and exterior siding. Heavy snowfall in western counties contrasts with salt-air exposure near the Atlantic, creating varied risk profiles across relatively short distances. Comparing Massachusetts homeowners insurance quotes allows residents to align coverage with both building characteristics and regional climate exposure rather than relying on a single statewide average.

How Much Does Homeowners Insurance Cost in Massachusetts?

The average cost of home insurance in Massachusetts is approximately $1,420 per year, or about $118 per month for $300,000 in dwelling coverage. Insurance pricing often reflects restoration labor costs, material availability, and claim history tied to winter storm damage more than population size alone. Coastal ZIP codes and multi-family structures may experience higher premiums, while newer inland developments sometimes see more moderate pricing. Reviewing several home insurance quotes provides clearer insight into neighborhood-specific rates and available savings opportunities.

Does Massachusetts Have the 80% Homeowners Insurance Rule?

When it comes to determining the payout for an approved insurance claim, insurance carriers typically follow the 80/20 rule. According to this rule, policyholders are required to maintain dwelling coverage that is at least 80% of the replacement cost value (RCV) of their home, as stated in their policy contract.

For instance, if the estimated replacement cost value (RCV) of your home is $450,000, your dwelling coverage should be no less than $360,000 (80% of $450,000). Failing to maintain su

Most insurance carriers operating in Massachusetts apply the 80% homeowners insurance rule as a standard industry practice rather than a state-issued mandate. This guideline typically requires homeowners to insure their dwelling for at least 80% of its estimated replacement cost in order to receive full reimbursement after a covered loss.

Replacement cost reflects what it would take to rebuild the home using similar materials and labor, not its resale value. Falling below this threshold can result in partial payouts, which is why periodic coverage reviews are recommended after renovations or rising construction expenses.

How to Find Home Insurance in Massachusetts

Finding property insurance in Massachusetts often involves evaluating structural age and proximity to water rather than just comparing premiums. Older homes, multi-family properties, and shoreline residences may have fewer carrier options than newer suburban builds. Working with an agency that can compare home insurance quotes in Massachusetts allows residents to review deductible structures, rebuilding estimates, and endorsements across multiple insurers. Homeowners who encounter underwriting limitations may also explore the Massachusetts FAIR Plan, which offers last-resort coverage for qualifying properties.

Preventative improvements can also influence eligibility and long-term pricing. Roof reinforcements, updated electrical wiring, sump pumps, and insulation upgrades are common measures that support favorable underwriting decisions. These updates can also reduce the likelihood of costly winter-related claims while improving property resilience.

fficient coverage may result in incomplete reimbursement from your insurer in case of a claim.

It’s crucial to keep in mind that the replacement cost value (RCV) of your home can be influenced by home improvements and inflation, which may impact overall replacement costs. Therefore, regular communication with your insurance agent is vital to ensure you have the appropriate level of coverage that accurately reflects the RCV of your home.

How Do Home Insurance Deductibles Affect Rates in Massachusetts?

Choosing a deductible is often a financial planning decision rather than a simple policy selection. Higher deductibles generally lower annual premiums because homeowners retain more responsibility, while lower deductibles increase monthly costs but reduce out-of-pocket expenses after a claim. In coastal counties, some home insurance policies may apply separate wind or hurricane deductibles depending on carrier guidelines.

Compare Home Insurance Rates by Coverage Levels in Massachusetts

Dwelling coverage is calculated using the projected cost to reconstruct the home, not its resale price, and insurance premiums generally increase as coverage amounts grow. Properties with historic features, custom materials, or multi-family configurations can require higher restoration budgets, which may influence policy pricing. The figures shown below represent broad statewide estimates rather than exact neighborhood-level quotes. Checking multiple home insurance quotes gives a more realistic view of potential costs.

| Dwelling Coverage | Average Annual Insurance Cost |

|---|---|

| $150,000 | $690 |

| $250,000 | $1,050 |

| $300,000 | $1,420 |

| $400,000 | $1,820 |

| $500,000 | $2,250 |

Is Home Insurance Tax Deductible in Massachusetts?

Homeowners insurance is generally not tax deductible for primary residences because it is considered a personal living expense. Exceptions may apply if part of the home is used exclusively for business purposes or if the property generates rental income.

Federally declared disaster losses that are not fully reimbursed may also qualify under certain circumstances. Because tax regulations vary by filing status and property use, consulting a licensed tax advisor is recommended.

Bundling Home and Auto Insurance in Massachusetts

Many property owners bundle home and auto insurance to streamline policy management and potentially reduce overall insurance expenses. Multi-policy discounts can align billing cycles, centralize claims administration, and help maintain consistent liability limits.

Bundling opportunities may also extend to umbrella or recreational vehicle policies depending on carrier offerings. InsureOne assists residents in comparing bundled options across multiple insurers to identify coverage solutions that balance value and protection.

What Factors Do Insurers Consider in Massachusetts?

Insurance pricing in Massachusetts reflects both structural and environmental variables that influence claim likelihood and repair costs. Because coastal and inland regions present different exposure profiles, pricing may vary even between nearby communities.

Key considerations include:

- Proximity to coastline or flood zones

- Roof age and building materials

- ZIP-code claim frequency and winter storm exposure

- Estimated rebuilding cost based on labor and materials

- Credit-based insurance score where permitted

- Presence of safety features such as alarms or water shut-off systems

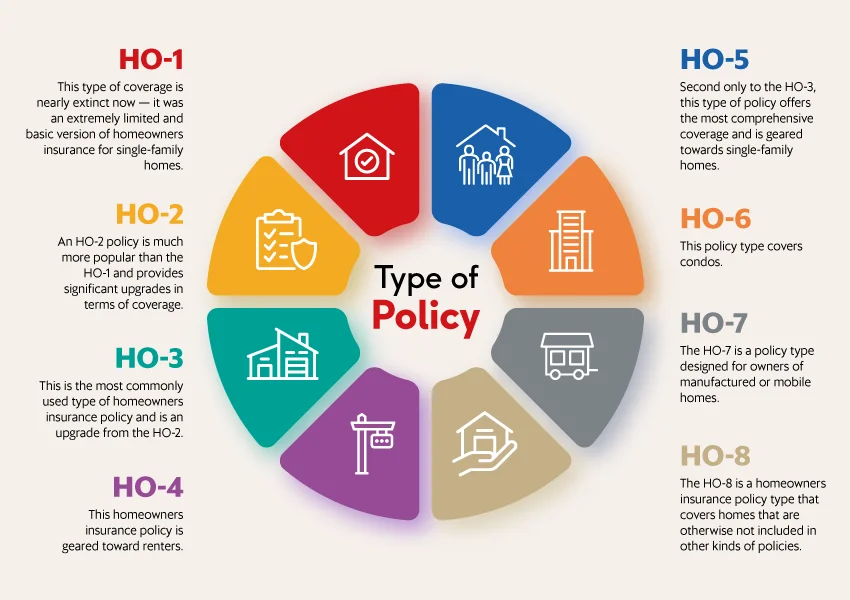

What Are the Different Types of Home Insurance?

Homeowners insurance is structured through several standardized policy formats designed to match ownership status and building design. Detached single-family homes most commonly use HO-3 policies, which balance structural protection with defined personal property coverage. Condominium owners typically rely on HO-6 coverage that works alongside association master policies, while renters select HO-4 insurance for belongings and liability. Older or historically significant homes sometimes require HO-8 valuation methods due to restoration material differences.

Massachusetts property owners frequently supplement base policies with endorsements shaped by regional conditions. Water-backup protection, ordinance or law coverage for code upgrades, and extended replacement cost endorsements are common additions, particularly for homes with basements or aging infrastructure.

What Is the Most Common Homeowners Insurance in Massachusetts?

The HO-3 policy remains the most widely selected homeowners insurance option because it balances comprehensive structural protection with flexible pricing. Coverage priorities may shift by region, with coastal homeowners evaluating wind or flood endorsements and inland properties focusing on basement-related coverage. Multi-family buildings sometimes review landlord-specific policies.

What Weather Affects Home Insurance Costs in Massachusetts?

Seasonal weather patterns significantly influence insurance premiums throughout the state. Winter storms, ice dams, and heavy snowfall are major considerations, particularly in western counties. Coastal regions may experience nor’easters, strong winds, and occasional tropical storm remnants. Localized flooding and lightning events can also contribute to claim frequency. Understanding these weather influences helps homeowners determine whether endorsements or separate flood coverage are appropriate.

What Does Homeowners Insurance Cover in Massachusetts?

Standard homeowners insurance policies in the state provide layered protection that extends beyond the physical structure of the home. Coverage typically applies to structural damage from covered perils as well as personal belongings and financial liability related to on-property incidents. Policy limits and deductibles influence reimbursement levels, making periodic reviews important as rebuilding costs change. Flood damage generally requires a separate flood insurance policy.

Most policies commonly include:

- Dwelling coverage for the home’s structure and attached systems

- Personal property coverage for interior belongings

- Liability protection for certain injury or property damage claims

- Additional living expenses (ALE) during covered repairs

- Other structures coverage for detached garages or sheds

Get the Best Homeowners Insurance in Massachusetts Today

Securing homeowners insurance in Massachusetts often involves balancing property age, coastal exposure, and long-term financial planning. InsureOne simplifies this process by reviewing multiple insurance carriers and presenting coverage options in a clear, organized format.

Homeowners can begin with a quick online quote, visit a nearby office, or speak with a licensed professional at 800-836-2240 for personalized guidance. With InsureOne, Massachusetts residents gain structured insight that turns complex insurance decisions into manageable choices.

FAQs

How much is homeowners insurance in Massachusetts?

The average cost in Massachusetts is about $1,420 per year, though actual pricing varies by ZIP code, home age, and rebuilding expenses. Coastal properties or multi-family homes may experience higher premiums due to restoration complexity and storm exposure. Seasonal weather patterns also influence annual rates. Exploring several home insurance quotes helps refine cost expectations for an individual residence.

Homeowners insurance is not mandated by state law for owner-occupied homes. However, mortgage lenders typically require a policy to protect their financial interest in the property. Even without a loan, many residents carry insurance because repair or rebuilding expenses after storms or fires can be substantial. Maintaining home insurance in Massachusetts offers both structural and liability protection.

Homeowners insurance is not mandated by state law for owner-occupied homes. However, mortgage lenders typically require a policy to protect their financial interest in the property. Even without a loan, many residents carry insurance because repair or rebuilding expenses after storms or fires can be substantial. Maintaining home insurance in Massachusetts offers both structural and liability protection.

What weather risks affect Massachusetts home insurance rates?

Insurance premiums are influenced by winter storms, nor’easters, coastal winds, and localized flooding. Homes near the shoreline may require additional endorsements or separate flood coverage. Seasonal storm exposure contributes to underwriting decisions. Insurers evaluate these risks carefully when calculating home insurance rates in the region.

What factors influence the cost of homeowners insurance in Massachusetts?

Insurers evaluate location, building materials, roof condition, and estimated replacement cost when determining premiums. Additional factors include deductible selection, prior claims history, and local building codes. Environmental exposure such as proximity to the coast or flood zones may also influence pricing. Reviewing options through InsureOne helps ensure these variables are compared across carriers.