New Jersey Homeowners Insurance Quotes

Everything You Need to Know About Home Insurance in New Jersey

New Jersey presents a distinctive housing landscape shaped by coastal communities, dense suburban neighborhoods, and historic town centers located between major metropolitan corridors. Homeowners may live in shorefront properties along the Atlantic, classic colonials in central counties, or multi-family brownstones closer to urban transit lines. Because property age, building materials, and proximity to water vary significantly across the state, insurance needs often differ from one ZIP code to another. Detached garages, finished basements, and older masonry construction are also common features that influence rebuilding costs and policy limits.

Climate exposure further distinguishes homeowners insurance in New Jersey from many inland states. Nor’easters, coastal flooding, and hurricane-related wind events can affect shoreline regions, while northern counties may experience heavier snowfall and ice accumulation during winter months. Seasonal storms and localized flooding also play a role in underwriting decisions. Exploring several New Jersey home insurance options makes it easier to align protection with a home’s structure and regional climate risks.

How Much Does Homeowners Insurance Cost in New Jersey?

The average cost of home insurance in the state is approximately $1,250 per year, or about $104 per month for $300,000 in dwelling coverage. While rates remain moderate compared to several coastal states, premiums have gradually shifted due to higher construction material pricing, labor expenses, and storm-related claims.

Pricing varies by ZIP code because insurers evaluate shoreline exposure, rebuilding costs, and access to emergency services. Reviewing multiple home insurance quotes provides clearer insight into location-specific pricing and potential discounts.

Does New Jersey Have the 80% Homeowners Insurance Rule?

Most insurance carriers in New Jersey apply the 80% homeowners insurance rule as a standard industry guideline. This principle typically requires homeowners to insure their dwelling for at least 80% of its estimated replacement cost to qualify for full reimbursement on covered losses. Replacement cost reflects the expense of reconstructing the home using similar materials and labor rather than its resale value.

Falling below this threshold can result in partial payouts even when damage is not total, which is why periodic coverage reviews are recommended after renovations or rising material costs.

How to Find Home Insurance in New Jersey

Obtaining property insurance in New Jersey is generally straightforward for newer homes in lower-risk inland areas, but shoreline properties or older structures may experience more limited carrier options. Working with an agency that can compare home insurance quotes in New Jersey increases visibility into deductible structures, endorsements, and rebuilding cost calculations across insurers.

Homeowners facing underwriting restrictions may also explore the New Jersey FAIR Plan, which offers last-resort coverage for qualifying properties. Reviewing multiple policies helps ensure coverage aligns with both property condition and environmental exposure.

Preventative improvements can also influence eligibility and long-term pricing. Reinforcing roofing materials, upgrading drainage systems, installing sump pumps, and elevating utilities in flood-prone areas are common risk-reduction measures. These steps not only support favorable underwriting decisions but can also minimize the likelihood of future claims.

How Do Home Insurance Deductibles Affect Rates in New Jersey?

Deductibles represent the portion of repair costs a homeowner agrees to pay before insurance coverage applies. Selecting a higher deductible generally lowers annual premiums because the policyholder assumes more financial responsibility, while lower deductibles increase monthly expenses but reduce out-of-pocket costs after a claim.

Some home insurance New Jersey policies may apply separate hurricane or wind deductibles in coastal areas depending on carrier guidelines. Determining the appropriate deductible often involves balancing premium savings with financial preparedness for unexpected repairs.

Compare Home Insurance Rates by Coverage Levels in New Jersey

Dwelling coverage is based on estimated rebuilding cost rather than market value, and premiums typically rise as coverage limits increase. Properties near the coastline or in densely populated counties may experience higher pricing due to restoration complexity and labor demand. The table below reflects statewide averages rather than precise ZIP-code quotes.

| Dwelling Coverage | Average Annual Insurance Cost |

|---|---|

| $150,000 | $610 |

| $250,000 | $880 |

| $300,000 | $1,250 |

| $400,000 | $1,590 |

| $500,000 | $1,980 |

Is Home Insurance Tax Deductible in New Jersey?

For most primary residences, homeowners insurance is treated as an everyday household cost and is not tax deductible. Still, deductions may be possible if part of the home is used solely for business or generates rental income, or if a federally declared disaster results in unreimbursed losses. Because tax laws shift and personal scenarios differ, professional advice can provide clearer direction.

Bundling Home and Auto Insurance in New Jersey

Many homeowners choose to bundle home and auto insurance to streamline policy management and potentially reduce overall insurance expenses. Multi-policy discounts can align billing cycles, centralize claims administration, and help maintain consistent liability limits. Bundling opportunities may also extend to umbrella or recreational vehicle policies depending on carrier offerings. InsureOne supports New Jersey residents in assessing multi-policy combinations across carriers to match financial value with appropriate protection.

What Factors Do Insurers Consider in New Jersey?

When determining home insurance rates in New Jersey, insurers evaluate both structural and environmental variables that influence claim likelihood and repair costs. Because coastal and inland regions present different risk profiles, pricing may vary even between nearby communities.

Key considerations include:

- Proximity to coastline or flood zones

- Roof age and building materials

- ZIP-code claim frequency and storm exposure

- Estimated rebuilding cost based on labor and materials

- Credit-based insurance score where permitted

- Presence of safety features such as alarms or water shut-off systems

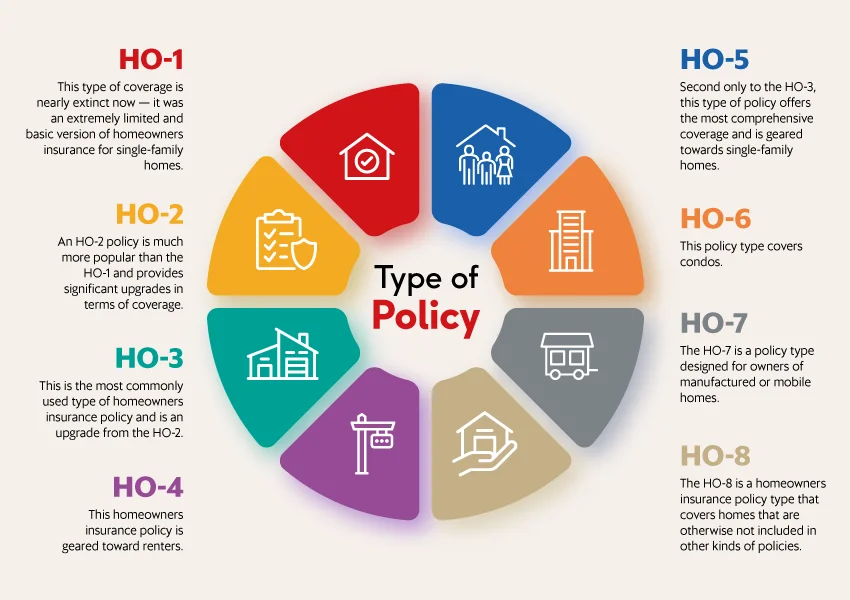

What Are the Different Types of Home Insurance?

Home insurance policies are organized by standardized HO forms that correspond to ownership status and property type. The HO-3 policy remains the most common option for single-family homes because it provides broad structural coverage alongside defined personal property protection. Homeowners seeking expanded protection may consider an HO-5 policy, while condominium owners typically rely on HO-6, renters use HO-4, and older or historically significant homes may require HO-8 valuation methods.

New Jersey homeowners often supplement base policies with endorsements tailored to regional conditions. Water-backup coverage, ordinance or law protection for code upgrades, and extended replacement cost endorsements are common additions, particularly for homes with basements or aging infrastructure. Reviewing both policy form and endorsements ensures alignment with the home’s structure and local risk patterns.

What Is the Most Common Homeowners Insurance in New Jersey?

The HO-3 policy continues to be the most widely selected homeowners insurance option due to its balance of comprehensive protection and flexible pricing. However, coverage needs vary based on proximity to water, property age, and weather exposure. Shoreline homeowners may prioritize wind or flood endorsements, while inland properties often focus on detached structure coverage. Comparing New Jersey homeowners insurance quotes allows homeowners to tailor policies to both environmental and structural considerations.

What Weather Affects Home Insurance Costs in New Jersey?

Seasonal weather patterns influence insurance premiums throughout the state. Coastal counties may experience hurricane-related winds and storm surge, while northern areas often encounter heavier snowfall and ice accumulation.

Spring thunderstorms and localized flooding can also contribute to claim frequency in certain regions. Evaluating these seasonal risks helps homeowners determine whether endorsements or separate flood coverage are appropriate.

What Does Homeowners Insurance Cover in New Jersey?

Standard homeowners insurance policies in New Jersey provide layered protection that extends beyond the building itself. Coverage typically applies to structural damage from covered perils as well as personal belongings and financial liability related to on-property incidents. Policy limits and deductibles influence reimbursement levels, making periodic reviews important as rebuilding costs change.

Most policies commonly include:

- Dwelling coverage for the home’s structure and attached systems

- Personal property coverage for interior belongings

- Liability protection for certain injury or property damage claims

- Additional living expenses (ALE) during covered repairs

- Other structures coverage for detached garages or sheds

Get the Best Homeowners Insurance in New Jersey Today

Choosing homeowners insurance in New Jersey often means weighing property coverage needs against regional weather exposure and future repair costs. InsureOne streamlines the search by reviewing multiple insurance carriers at once and organizing policy options in a clear, side-by-side format so homeowners can make informed decisions with confidence.

Homeowners can begin with a quick online quote, visit a nearby office for personalized assistance, or call 800-836-2240 to speak with a licensed insurance professional. With InsureOne, New Jersey residents gain informed guidance and coverage solutions designed to reflect the state’s diverse property styles and climate conditions.

FAQs

How much is homeowners insurance in New Jersey?

The average cost of homeowners insurance in New Jersey is about $1,250 per year, though actual pricing varies by ZIP code, home age, and rebuilding expenses. Coastal properties or older masonry homes may experience higher premiums. Seasonal weather exposure also influences annual rates.

Is homeowners insurance required in New Jersey?

Homeowners insurance is not mandated by state law for owner-occupied homes. However, mortgage lenders typically require a policy to protect their financial interest in the property. Even without a loan, many residents carry insurance because repair or rebuilding expenses after storms or fires can be substantial. Maintaining home insurance in New Jersey offers both structural and liability protection.

What weather risks affect New Jersey home insurance rates?

Insurance premiums in New Jersey are influenced by coastal storms, hurricane-related winds, winter snowfall, and localized flooding. Homes near the shoreline may require additional endorsements or separate flood coverage. Seasonal storm exposure contributes to underwriting decisions. Insurers assess these risks carefully when calculating home insurance rates in the area.

What factors influence the cost of homeowners insurance in New Jersey?

Insurers evaluate location, building materials, roof condition, and estimated replacement cost when determining premiums. Additional factors include deductible selection, prior claims history, and local building codes. Environmental exposure such as proximity to the coast or flood zones may also influence pricing. Reviewing options through InsureOne helps ensure these variables are compared across carriers.