Ohio Homeowners Insurance Quotes

Everything You Need to Know About Home Insurance in Ohio

Ohio offers a wide range of living environments, from large metropolitan cities to quiet rural farmland and lakefront communities along Lake Erie. Major cities such as Columbus, Cleveland, and Cincinnati provide strong employment markets and cultural attractions, while smaller towns often appeal to homeowners seeking affordability and space. Housing styles vary across the state and include historic brick homes, mid-century ranch houses, modern subdivisions, and properties with detached garages or workshops. Because property values and rebuilding costs differ from one region to another, insurance needs can vary significantly by ZIP code.

The states four-season climate also introduces weather-related risks that make homeowners insurance in Ohio an essential financial safeguard. Winter snow and ice can lead to frozen pipes and roof damage, while spring and summer storms may bring wind, hail, and occasional tornado activity. Flooding near rivers and low-lying areas is another consideration and typically requires separate flood insurance coverage. Comparing Ohio homeowners insurance quotes helps ensure policies align with both property characteristics and regional weather exposure.

How Much Does Homeowners Insurance Cost in Ohio?

The average cost of home insurance in the state is approximately $1,420 per year, or about $118 per month for $300,000 in dwelling coverage. This amount is generally lower than the national average, but premiums have gradually increased due to inflation, higher construction material costs, and more frequent severe weather claims.

Rates vary by ZIP code because insurers evaluate local rebuilding expenses, contractor availability, and proximity to emergency services. Comparing home insurance Ohio quotes provides a clearer picture of pricing based on both property value and location.

Does Ohio Have the 80% Homeowners Insurance Rule?

Yes, most insurance carriers operating in the region apply the 80% homeowners insurance rule as a standard industry practice. This guideline typically requires homeowners to insure their dwelling for at least 80% of its estimated replacement cost to qualify for full reimbursement after a covered loss.

Replacement cost reflects the expense of rebuilding the structure using similar materials and labor rather than the home’s market value. Falling below this threshold may result in reduced claim payouts even when damage is partial rather than total.

How to Find Home Insurance in Ohio

Most homeowners can obtain property insurance in Ohio through traditional insurance carriers, but older homes, prior claims, or properties located in higher-risk flood zones may limit available options. Working with an agency that can compare home insurance quotes in Ohio often improves both pricing and coverage availability because insurers evaluate risk differently.

Homeowners who encounter limited private-market choices may also explore the Ohio FAIR Plan, which can provide last-resort coverage for eligible properties. Comparing multiple quotes helps ensure coverage reflects both property condition and regional risk factors.

Taking proactive steps to reduce risk can also strengthen eligibility and help maintain competitive premiums. Common improvement strategies include updating roofing materials, reinforcing gutters and drainage systems, installing sump pumps in basements, and adding water-backup protection. Maintaining updated electrical and plumbing systems may also influence underwriting decisions and long-term pricing. These upgrades not only support insurance approval but also reduce the likelihood of costly claims over time.

How Do Home Insurance Deductibles Affect Rates in Ohio?

A deductible is the portion of a claim a homeowner agrees to pay out of pocket before insurance coverage applies. Higher deductibles typically lower annual premiums, while lower deductibles increase monthly costs but reduce immediate financial responsibility after a covered loss.

Some policies may include separate wind or hail deductibles depending on regional storm exposure and insurer guidelines. Selecting a deductible involves balancing premium savings with the ability to manage unexpected repair expenses.

Compare Home Insurance Rates by Coverage Levels in Ohio

Dwelling coverage is based on estimated rebuilding cost rather than market value, and premiums generally rise as coverage limits increase. Local homeowners may see pricing differences due to home age, construction materials, and localized storm exposure.

The table below reflects statewide averages and should be viewed as general guidance rather than exact ZIP-code pricing. Comparing multiple Ohio homeowners insurance quotes provides a clearer understanding of cost differences across coverage levels.

| Dwelling Coverage | Average Annual Insurance Cost |

|---|---|

| $150,000 | $780 |

| $250,000 | $1,060 |

| $300,000 | $1,420 |

| $400,000 | $1,780 |

| $500,000 | $2,140 |

Bundling Home and Auto Insurance in Ohio

Finding the best protection for your home is vital. But it never hurts to get a good deal at the same time. One way you can lower your annual premium is through discounts, including bundling.

Bundling is purchasing two or more insurance lines with the same insurer. For example, if you bundle your home coverage with your car insurance, you could get up to 25% off. Also known as a multi-policy discount, your carrier will reward you for being loyal and trusting them with your needs.

For those who enjoy taking the family out on the boat at Lake Erie, you can find affordable boat insurance in Ohio. Likewise, those who enjoy taking the bike out for a thrilling adventure on Ohio’s Windy 9 in Athens or the Triple Nickle in Zanesville, need the best motorcycle insurance in Ohio.

With bundling, policies and claims are easier to manage and administer. Your annual renewal (or six-month) will also be easier to keep track of when you use one company.

Bundling Home and Auto Insurance in Ohio

Bundling home and auto insurance allows homeowners to place multiple policies with the same insurer for simplified management and potential savings. Many carriers offer multi-policy discounts that can reduce overall insurance expenses while aligning billing cycles and renewal dates.

Bundling may also help maintain consistent liability limits and reduce administrative complexity across policies. InsureOne helps Ohio homeowners compare bundled options across multiple carriers to find coverage that balances value and long-term protection.

What Factors Do Insurers Consider in Ohio?

Insurance providers evaluate several variables when determining home insurance rates in Ohio, beginning with the property’s structure, location, and estimated rebuilding cost. Insurers also consider how quickly emergency services can respond and whether the home has safety or mitigation features installed.

Regional weather exposure and prior claims history further influence underwriting decisions and overall premium levels. Because these factors vary across counties, two similar homes may receive noticeably different quotes.

Common underwriting considerations include:

- ZIP code and neighborhood risk levels, including prior claim frequency

- Age of the home and roof condition

- Construction materials and total square footage

- Proximity to fire hydrants and fire stations

- Estimated replacement or rebuilding cost

- Credit-based insurance score, where permitted by law

- Presence of safety devices, such as alarm systems or water shut-off valves

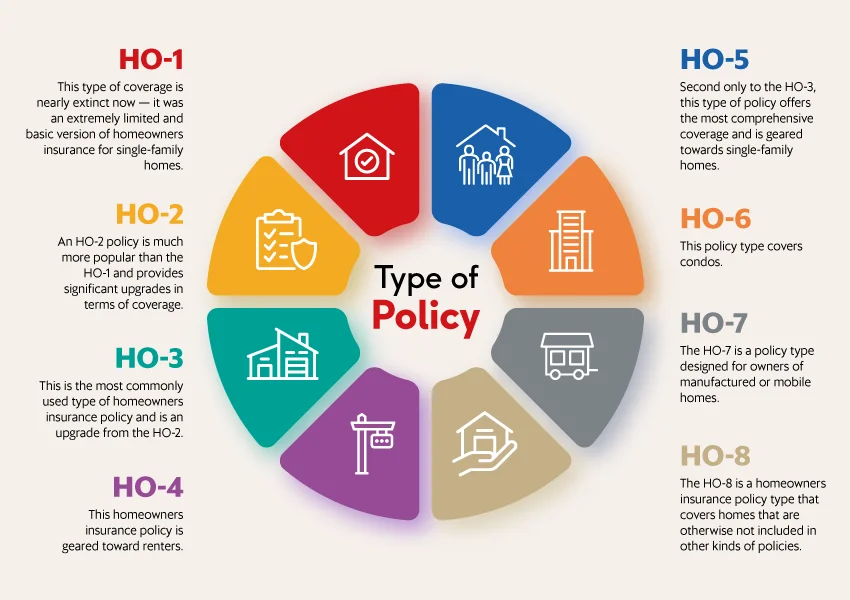

What Are the Different Types of Home Insurance?

Home insurance policies are organized by standardized HO forms that correspond to ownership status and structure type. The HO-3 policy is the most common choice for single-family homes because it offers broad structural protection and defined personal property coverage. Homeowners seeking more comprehensive protection may consider an HO-5 policy, which expands coverage for both the dwelling and personal belongings. Other common forms include HO-6 for condominium owners, HO-4 for renters, HO-7 for manufactured homes, and HO-8 for older or historic properties that require specialized valuation methods.

Beyond selecting a base policy form, many Ohio homeowners add endorsements that reflect local risks and property features. Water-backup coverage, extended replacement cost, and ordinance or law endorsements are frequently chosen for homes with basements or aging construction. These additions help close potential coverage gaps that may not be fully addressed under standard policies. Reviewing both the policy form and endorsements ensures coverage aligns with the home’s structure, location, and long-term financial goals.

What Is the Most Common Homeowners Insurance in Ohio?

The HO-3 policy remains the most widely selected homeowners insurance option in the state due to its balance of comprehensive protection and practical pricing. However, coverage needs vary based on property age, location, and weather exposure across the state.

Urban homes may prioritize water-backup endorsements, while rural properties often require added protection for detached structures. Comparing Ohio homeowners insurance quotes helps ensure policies match both the home and its regional risk profile.

What Weather Affects Home Insurance Costs in Ohio?

Local weather patterns influence insurance premiums because insurers evaluate the likelihood and severity of weather-related claims. Winter snow and ice can lead to frozen pipes and roof stress, while spring and summer storms may bring wind damage and hail. Tornado activity, although not constant, contributes to regional underwriting considerations in

certain counties. Flooding near rivers and low-lying areas remains a significant concern and typically requires separate flood insurance coverage.

What Does Homeowners Insurance Cover in Ohio?

Standard homeowners insurance policies in Ohio are designed to protect both the physical structure of the home and the homeowner’s financial liability after covered events. Coverage typically applies to risks such as fire, wind, hail, and certain types of accidental water damage depending on the policy form selected.

Policies also include financial protections that extend beyond the building itself, which is why reviewing limits and deductibles is important. Flood damage is excluded from standard policies and requires a separate flood insurance plan.

Most policies commonly include the following protections:

- Dwelling coverage for the home’s structure and attached systems

- Personal property coverage for belongings such as furniture, clothing, and electronics

- Liability protection for certain injury or property damage claims involving visitors

- Additional living expenses (ALE) if temporary housing is required after a covered loss

- Other structures coverage for detached garages, sheds, or fences

Many homeowners also add endorsements such as water-backup protection, ordinance or law coverage for code upgrades, or extended replacement cost to better reflect rebuilding expenses and regional weather exposure.

Get the Best Homeowners Insurance in Ohio Today

Protecting a home in Ohio begins with coverage that reflects regional risks, rebuilding costs, and long-term financial goals. InsureOne simplifies the process by comparing multiple insurance carriers to present clear policy options and flexible deductibles tailored to homeowners.

Start with a quick online quote, visit a nearby office for personalized support, or call 800-836-2240 to speak with a licensed insurance professional. With InsureOne, homeowners gain knowledgeable guidance and confidence that their coverage aligns with Ohio’s diverse housing and seasonal weather conditions.

FAQs

How much is homeowners insurance in Ohio?

The average cost of homeowners insurance in Ohio is approximately $1,420 per year, though actual pricing varies by ZIP code and property characteristics. Homes with higher replacement costs or increased storm exposure may see higher premiums than statewide averages. Insurers also consider roof age, claims history, and rebuilding expenses when determining rates. Comparing Ohio homeowners insurance quotes provides the most accurate estimate for a specific property.

Is homeowners insurance required in Ohio?

Homeowners insurance is not legally required by the state for owner-occupied homes. However, mortgage lenders typically require a policy as part of loan conditions to protect their financial interest. Even homeowners without mortgages often carry insurance because repair or rebuilding costs after storms or fires can be substantial. Maintaining home insurance provides both property and liability protection.

What weather risks affect Ohio home insurance rates?

Insurance premiums are influenced by seasonal weather patterns that increase claim frequency and repair costs. Winter storms and freezing temperatures can lead to roof damage and burst pipes, while spring and summer storms may bring wind and hail losses. Tornado activity also contributes to underwriting considerations in certain regions. Flooding near rivers or low-lying areas requires separate coverage since it is not included in standard policies.

What factors influence the cost of homeowners insurance in Ohio?

Insurers evaluate multiple elements when determining home insurance Ohio premiums, including location, home age, building materials, and estimated rebuilding cost. Additional factors include roof condition, proximity to fire services, claims history, and deductible choice. Regional weather exposure and local building codes may also influence pricing. Reviewing options through InsureOne helps ensure these variables are compared across multiple carriers.