Wisconsin Homeowners Insurance Quotes

Everything You Need to Know About Home Insurance in Wisconsin

Wisconsin living often revolves around water, seasons, and space. With thousands of lakes, wooded northern counties, agricultural land, and growing metropolitan hubs like Milwaukee and Madison, homeowners encounter a broad range of property styles and rebuilding considerations. Lakefront cottages, suburban single-family homes, historic brick duplexes, and rural farm properties each present different insurance requirements, which is why homeowners insurance policies are rarely uniform across the state. Construction materials, distance to emergency services, neighborhood density, and regional labor costs can all influence how coverage is structured and priced.

Seasonal weather is another defining factor for property planning. Heavy winter snowfall, spring thaw flooding , summer hailstorms, and occasional tornado activity can affect roof longevity, drainage systems, and structural repair costs. Even homes outside major flood zones may evaluate water-backup or sump-pump endorsements due to melting snow patterns and basement moisture concerns. Older homes with original plumbing or electrical systems may also review code-upgrade endorsements to account for modernization expenses after a loss. Because weather cycles, housing inventory, and construction expenses continue to evolve, maintaining appropriate home insurance in Wisconsin coverage is an important component of long-term financial protection.

With InsureOne, Wisconsin property owners can view multiple home insurance options in one place, helping them make confident coverage choices without feeling restricted to one insurer.

How Much Does Homeowners Insurance Cost in Wisconsin?

The average cost of home insurance policies in the state is approximately $1,780 per year, or about $148 per month, for a home insured with $300,000 in dwelling coverage. This rate remains slightly below the national average, but pricing varies depending on roof age, insulation quality, and regional weather exposure. Homes in northern counties with heavier snowfall may encounter different underwriting criteria than properties in southern metropolitan areas.

Insurance premiums are not identical across ZIP codes, and location continues to be one of the strongest pricing variables. Older homes, lake-adjacent properties, and houses with specialized materials may require higher rebuilding budgets, which can influence final policy costs.

How to Find Home Insurance in Wisconsin

Finding the right home insurance in Wisconsin begins with understanding how climate and property characteristics influence carrier participation and pricing. Homes near lakes or rivers may evaluate additional water-related endorsements, while inland suburban properties often have broader insurer availability. Comparing insurance quotes side-by-side allows homeowners to review deductible options, coverage limits, and endorsements without navigating multiple applications separately.

Risk-reduction improvements can also affect long-term eligibility. Updated roofing materials, reinforced gutters, modern electrical systems, and improved attic insulation may support more favorable underwriting outcomes. Independent agencies such as InsureOne simplify the process by presenting policy options from multiple insurers simultaneously, helping residents focus on coverage alignment rather than brand restriction.

How Do Home Insurance Deductibles Affect Rates in Wisconsin?

Deductibles represent the amount a homeowner agrees to pay toward a covered repair before insurance benefits begin, and they directly influence premium amounts. Selecting a higher deductible generally lowers annual costs because the policyholder retains more financial responsibility upfront, while choosing a lower deductible increases monthly expenses but reduces immediate out-of-pocket costs after a claim.

For example, if a homeowner selects a $2,000 deductible and incurs $8,000 in hail damage, the insurer would typically cover $6,000 once the deductible is met, subject to policy limits. In snow-heavy or storm-active regions, some carriers may apply separate wind or hail deductibles that differ from the standard deductible listed on the declarations page.

Compare Home Insurance Rates by Coverage Levels in Wisconsin

Dwelling coverage is based on projected rebuilding expenses rather than resale market value, and premiums generally increase as coverage limits rise. Homes with custom woodwork, lakefront exposure, or multi-unit layouts may require higher restoration budgets, which can influence insurance pricing. The figures below represent statewide averages rather than exact neighborhood-level quotes. Reviewing multiple homeowners insurance options provides a more accurate estimate for personalized costs.

| Dwelling Coverage | Average Annual Insurance Cost |

|---|---|

| $100,000 | $720 |

| $200,000 | $1,140 |

| $300,000 | $1,780 |

| $400,000 | $2,310 |

| $500,000 | $2,950 |

Is Home Insurance Tax Deductible in Wisconsin?

For most primary residences, home insurance premiums are not tax deductible because they are considered personal living expenses. There are, however, limited circumstances where portions of related expenses may qualify depending on how the property is used and how the loss occurred. Because eligibility depends on individual filing status and documentation, professional tax guidance is recommended before applying deductions.

Situations where partial deductions may apply include:

- A dedicated home office used exclusively for business purposes

- Rental income generated from part of the property

- Federally declared disaster losses that were not fully reimbursed

- Certain casualty-loss scenarios tied to qualifying natural events

Does Wisconsin Have the 80% Homeowners Insurance Rule?

Many homeowners policies use what is commonly called a coinsurance requirement, which typically expects the insured dwelling limit to represent a large percentage of the home’s estimated rebuild value. When coverage falls too far below that benchmark, an insurer may reduce the payout amount on structural claims even if the loss itself is covered. The purpose of this guideline is to encourage policy limits that realistically reflect construction costs rather than outdated purchase prices.

As an illustration, if reconstruction estimates place a home near $350,000, carrying substantially less coverage could result in only a portion of repair expenses being reimbursed after a major loss. Building costs do not remain static — contractor availability, lumber and material pricing, and remodeling projects can all shift replacement values over time. Periodic policy reviews help ensure the insured amount keeps pace with current market conditions so coverage remains proportional to potential rebuild expenses.

Bundling Home and Auto Insurance in Wisconsin

Many residents choose to bundle home insurance with auto coverage to simplify policy management and potentially reduce overall insurance expenses. Multi-policy discounts often align billing cycles, centralize claims handling, and help maintain consistent liability limits across policies. In addition to potential savings, bundling can make renewals and documentation easier to track because homeowners work with one insurer instead of several.

Bundling opportunities may also extend to motorcycles, boats, or personal umbrella policies depending on insurer offerings. InsureOne assists residents in reviewing bundled Wisconsin homeowners insurance quotes across multiple carriers to identify policy combinations that balance financial value with long-term protection needs.

What Weather Affects Home Insurance Costs in Wisconsin?

Weather patterns play a major role in pricing because seasonal conditions can influence claim frequency and repair costs. Heavy winter snowfall and ice accumulation can contribute to roof strain, frozen pipes, and ice-dam formation. Spring thaw and rainfall may create localized flooding or basement seepage concerns, even in areas not designated as high-risk flood zones. Summer hailstorms and strong winds can result in siding and roof damage, while occasional tornado activity may prompt separate wind deductibles depending on county exposure. Understanding these variables helps homeowners evaluate whether endorsements or separate flood policies are appropriate.

What Factors Do Insurers Consider in Wisconsin?

Home insurance companies set premiums by looking at how expensive a property would be to repair or rebuild and how likely it is to experience damage. Details such as square footage, electrical and plumbing systems, exterior materials, roof lifespan, and neighborhood fire-protection access all contribute to how a policy is priced. Many carriers also review an applicant’s previous claim record and credit-based insurance score to gauge overall risk consistency. These combined data points help insurers determine both eligibility and final premium ranges.

In Wisconsin, additional influences often relate to regional climate and infrastructure patterns rather than just the structure itself. Residences near lakes or rivers may prompt closer review of moisture exposure, while areas known for prolonged winter accumulation or frequent hail can affect deductible structures and coverage recommendations. Local building codes and permit requirements may also raise projected reconstruction costs, especially for older homes needing upgrades to meet current standards. Properties that have recently added energy-efficient insulation, impact-resistant shingles, or reinforced drainage systems sometimes receive more favorable underwriting consideration compared to houses with aging components.

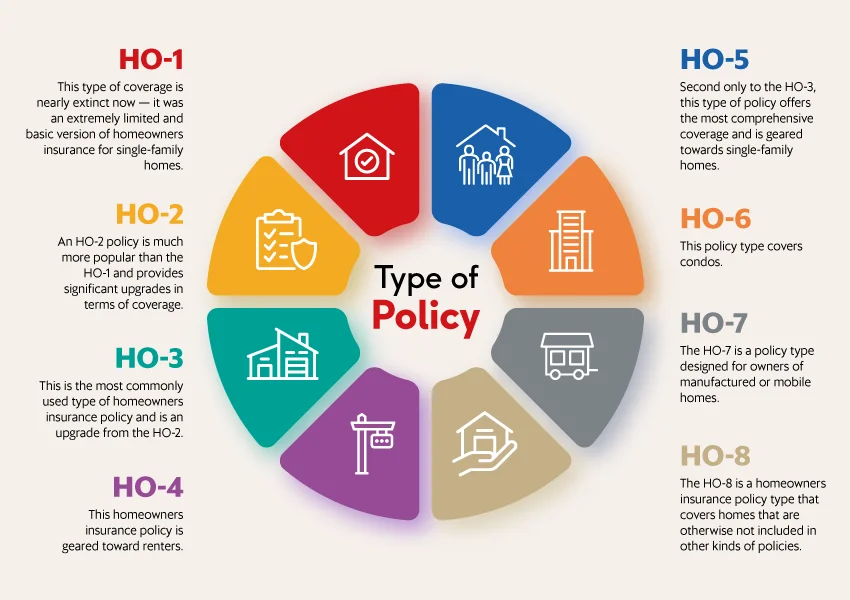

What Are the Different Types of Home Insurance?

Home insurance policies are organized through standardized HO forms that correspond to ownership structure and property type rather than architectural style alone. The HO-3 policy is the most commonly selected option for single-family homes because it provides broad dwelling protection alongside defined personal property coverage. Homeowners seeking expanded personal belongings protection may consider HO-5 coverage, while condominium owners typically rely on HO-6, renters use HO-4, and manufactured homes often require HO-7 policies due to construction differences. Residents frequently evaluate endorsements such as water-backup coverage, ordinance or law protection for code upgrades, and extended replacement cost options.

What Is the Most Common Homeowners Insurance in Wisconsin?

Among the various homeowners policy formats available, the HO-3 form is commonly chosen because it delivers broad protection for the dwelling while also including personal belongings and liability coverage under one structure. Even so, the ideal policy can shift depending on how the home was built, how old major systems are, and what environmental exposures exist in the surrounding area.

Properties near lakes or rivers frequently explore supplemental water-damage options, whereas homes in high-snow zones may pay closer attention to wind, hail, or roof deductibles. Evaluating local risk patterns helps homeowners fine-tune coverage limits and optional endorsements so the policy better reflects real-world conditions.

Get the Best Homeowners Insurance in Wisconsin Today

Choosing homeowners insurance in Wisconsin is less about picking a single policy and more about aligning coverage with how the property is built, where it is located, and how weather patterns may affect future repair costs. Rather than sorting through individual carrier websites, many residents prefer a comparison approach that highlights coverage differences, deductible structures, and pricing side-by-side. InsureOne brings these options together in one streamlined view, allowing homeowners to evaluate protection levels and budget considerations without limiting themselves to a single insurer.

Get started with a quick online quote, speak with a licensed insurance professional by phone at 800-836-2240, or visit a local office for personalized assistance. With access to several carriers and customizable coverage structures, InsureOne helps Wisconsin residents secure protection that aligns with both property value and regional risk conditions.

FAQs

How Much Is Homeowners Insurance in Wisconsin?

Homeowners insurance prices across Wisconsin often trend lower than the U.S. average, yet actual premiums shift noticeably based on neighborhood risk profiles and property features. Factors such as the age of the roof, heating efficiency, and recent renovations can influence how carriers calculate replacement expenses. Homes located near large bodies of water or in areas with prolonged winter accumulation may see different coverage recommendations than properties in dense urban corridors.

Is Home Insurance Required in Wisconsin?

Wisconsin statutes do not universally obligate homeowners to purchase insurance, yet lenders almost always require an active policy before approving or maintaining a mortgage. For owners without a loan, coverage is still commonly maintained because it offsets the financial impact of fire damage, storm losses, liability claims, and short-term relocation costs after a covered incident. Repair expenses can escalate quickly when structural components, roofing, or mechanical systems are involved. In practice, homeowners insurance in Wisconsin operates as a financial protection strategy rather than a state-mandated requirement.

What Weather Risks Affect Home Insurance in Wisconsin?

Insurance pricing is influenced by winter snow accumulation, spring thaw flooding, summer hailstorms, and occasional tornado activity. Ice dams and frozen pipes are also common seasonal considerations for underwriting. Flood damage is not included in standard homeowners policies and typically requires a separate flood insurance plan. These factors collectively shape deductible structures and overall homeowners insurance premiums.

What Factors Influence Home Insurance Rates in Wisconsin?

Home insurance pricing in Wisconsin is shaped by a combination of property characteristics and regional risk exposure rather than a single fixed formula. Insurers often review the home’s age, square footage, electrical and plumbing systems, and how costly local labor and materials would be if a rebuild were necessary. Geographic considerations — such as distance to fire departments, lake or river proximity, snowfall accumulation patterns, and neighborhood claim frequency — can also shift premium ranges.